This article was co-authored by wikiHow Staff. Our trained team of editors and researchers validate articles for accuracy and comprehensiveness. wikiHow's Content Management Team carefully monitors the work from our editorial staff to ensure that each article is backed by trusted research and meets our high quality standards.

This article has been viewed 24,167 times.

Learn more...

If you're a US homeowner, you may be able to get a break on your taxes by deducting the interest you paid on your mortgage. Some lower-income taxpayers also may be eligible for a credit for mortgage interest paid. The deduction reduces your taxable income, while the credit directly reduces the taxes that you owe. If you are able to claim both, your deduction is reduced by the amount of your credit.[1] Before you claim a mortgage interest deduction, however, do the math to make sure you'll really benefit from it. With the passage of the Tax Cuts and Jobs Act, most homeowners have greater tax savings by taking the standard deduction.[2]

Steps

Method 1

Method 1 of 3:Calculating Your Mortgage Interest Deduction

-

1Confirm that your mortgage interest qualifies. You can deduct interest paid on secured debt to purchase a home that has sleeping, cooking, and toilet facilities. Only interest on mortgages for your primary or second home qualifies.[3]

- If you took out a personal loan to buy a house with cash, you can't deduct the interest because the loan isn't secured by the property.

- If you own a second home, such as a summer home, and rent it out most of the time, it will likely be considered an investment property rather than a home. You cannot deduct mortgage interest for investment properties as an itemized deduction on your personal taxes. However, you may be able to deduct this interest to offset income from the property, if you are a real estate investor. Since this is a more complex situation, talk to a tax professional.

Tip: For tax years prior to 2018, you could also deduct interest from a home equity loan, such as a second mortgage or a HELOC (home equity line of credit). As of 2018, interest on these types of loans is no longer deductible unless you used the funds exclusively for home improvements.

-

2Review your copy of IRS Form 1098. Your mortgage lender will mail you IRS Form 1098, titled "Mortgage Interest Statement." You should receive this form by January 31 of the year in which you're filing your taxes. This form reports the total amount of your mortgage and amount of interest you paid in the previous year.[4]

- If you took out your mortgage after October 13, 1987, you can only deduct interest paid on up to $750,000 of debt. For mortgages taken out prior to that date, you can deduct interest paid on up to $1 million of debt.

- You can determine the basic amount of deductible interest from Form 1098. For example, suppose you took out a mortgage on your home for $200,000. Form 1098 shows that you paid $8,934 in interest. Since your mortgage is below $750,000, you can deduct the full $8,934 in interest you paid.

- Your mortgage lender also sends a copy of this form to the IRS. You don't have to submit the form with your taxes. However, you should keep it with your tax records in the event of an audit.

-

3Add points to your deduction over the life of your mortgage. Mortgage points are fees you pay to your mortgage lender at closing to reduce your interest rate. Since points represent prepaid interest, you generally can't deduct them in the year you pay them. Rather, you would spread them out and deduct an equal amount for each year through the life of your loan.[5]

- For example, suppose you took out a 20-year mortgage loan for $100,000 in 2018 and paid $4,800 in points. You made 3 monthly mortgage payments in 2018. You would divide $4,800 by 240 months to get $20, the amount you could deduct per month. Since you made 3 mortgage payments, you could deduct an additional $60 on your 2018 taxes.

- In some situations, you may be able to fully deduct the points you paid in the year that you paid them. This is only allowed if the mortgage is on your primary home and several other conditions are met. Talk to a tax professional before deducting your points in the year that you paid them.

-

4Compare your mortgage interest deduction to the standard deduction. Once you've totaled your mortgage interest deduction, check the standard deduction you would qualify for. If your mortgage interest deduction is less than your standard deduction, it doesn't make good financial sense to deduct your mortgage interest on your taxes.[6]

- Keep in mind that the mortgage interest deduction is not a 1-to-1 tax break. If you are in the 24 percent tax bracket and spend $12,000 in mortgage interest, you would only save $2,800 on your taxes. This is approximately the same amount you would save if you took the standard deduction.

- You can also use an online tax benefits calculator, such as the one at https://www.mortgagecalculator.org/helpful-advice/home-ownership-tax-benefits.php, to easily calculate your mortgage interest deduction.

- Unless you have significant other itemized deductions, your standard deduction will likely be greater than your mortgage interest deduction.

Method 2

Method 2 of 3:Taking a Mortgage Interest Deduction

-

1Use Form 1040 for your tax return. When it comes time to do your taxes, report your income on Form 1040. You can either download the form from the IRS website or use commercial tax preparation software.[7]

- Form 1040 is available at https://www.irs.gov/pub/irs-pdf/f1040.pdf if you want to complete your tax return manually. Make sure you download the form for the right tax year. For example, if you're filing taxes in 2019, you need the form for the 2018 tax year.

-

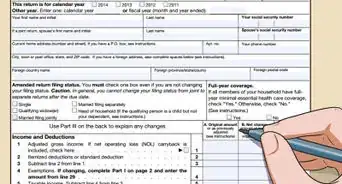

2Complete Schedule A to itemize your deductions. Calculate and report your itemized deductions on Schedule A. Tax preparation software typically will auto-populate this form based on your answers to questions about your mortgage interest and other itemized deductions.[8]

- If you're completing your tax returns by hand, you can download Schedule A at https://www.irs.gov/pub/irs-pdf/f1040sa.pdf.

Tip: If you use commercial tax preparation software, it typically will let you know if your itemized deductions are less than your standard deduction and recommend that you take the standard deduction.

-

3Copy interest paid from Form 1098 to Line 8a on Schedule A. Box 1 on Form 1098 lists the interest that you paid in that year. Box 6 lists the points paid on the purchase. If you are spreading points evenly over the life of the loan, divide that amount by the total number of months in your loan, then multiply by the number of monthly payments you made that year. Add this amount to the amount in Box 1, then write the total on Line 8a.[9]

- If you didn't use all of the loan for a home purchase or home improvements, check the box on Line 8 and follow the instructions that accompany Schedule A to determine how much of your interest is deductible.

-

4Fill in your other itemized deductions. Review the categories on Schedule A and determine what other itemized deductions you may have for that tax year. Only deduct amounts you can back up with receipts or other proof. Keep those documents with your other tax records.[10]

-

5Transfer your total itemized deductions to Line 8 of Form 1040. Add up all of your itemized deductions and fill in the total on Line 17 of your Schedule A. The same amount goes on Line 8 of your Form 1040.[11]

- If you are choosing to take itemized deductions even though they are less than your standard deduction, you must also check the box on Line 18 of Schedule A.

Method 3

Method 3 of 3:Claiming the Mortgage Interest Credit

-

1Receive a Mortgage Credit Certificate (MCC) from your state or local government. MCCs are issued to low-income individuals in connection with a new mortgage you took out to purchase your primary residence. Your state or local housing finance agency will have information on the availability of MCCs in your area and whether you qualify for one.[12]

- You must connect with your state or local housing finance agency and apply for the MCC program before you get a mortgage and buy your home. They aren't available for existing mortgages.

- An MCC shows the certified credit rate that you will use to calculate your credit, as well as your certified indebtedness amount. If your mortgage is higher than that amount, you can only use the interest paid on that amount for the purposes of the mortgage interest credit. You still may be able to deduct other interest you paid as an itemized deduction.

-

2Calculate the credit you're entitled to take on Form 8396. If you're doing your taxes by hand, download a copy of Form 8396 at https://www.irs.gov/pub/irs-pdf/f8396.pdf. Enter the interest you paid on Line 1. If your mortgage loan is less than the certified indebtedness amount shown on your MCC, you can enter all of the interest you paid over the course of the year. Otherwise, you can only enter the portion of your paid interest that applies to the lesser amount.[13]

- For example, if you have a certified indebtedness amount of $100,000, but your mortgage loan is for $125,000, you can only count 80 percent of the interest you paid towards the credit (since $100,000 is 80 percent of $125,000). If you paid $7,500 in interest, you would enter $6,000 on Line 1 of Form 8396.

- Enter the credit rate shown on your MCC on Line 2. If that rate is 20 percent or less, multiply Line 1 by Line 2 to find your mortgage interest credit. If the rate is higher than 20 percent, or if you refinanced your mortgage, follow the instructions on the form to calculate your credit.

Tip: If you refinance a mortgage for which you had an MCC, you must get a new MCC for the refi – otherwise, you won't be able to claim the credit.

-

3Attach Form 8396 to your Form 1040. Once you've calculated your mortgage interest credit, enter the amount on Line 54 of Form 1040, Schedule 3. If you're filing Form 1040-NR, enter the amount of your credit on Line 51. Check box "c" on the same line and enter "8396" in the space next to the box. Form 8396 must be submitted to the IRS as part of your tax return.[14]

- If you are also deducting mortgage interest on Schedule A of Form 1040, you must reduce the amount of interest you deducted by the amount on Line 3 of your Form 8396.

Warnings

- This article deals with the deduction of mortgage interest on US taxes. If you live in another country, your tax laws will be different. Consult a local tax attorney, accountant, or other tax professional.Thanks!

- The itemized deduction for mortgage insurance premiums expired at the end of 2017.[15]Thanks!

References

- ↑ https://help.creditkarma.com/hc/en-us/articles/360000021443-What-s-the-difference-between-the-Mortgage-Interest-Credit-and-the-Home-Mortgage-Interest-Deduction-

- ↑ https://www.investopedia.com/articles/mortgages-real-estate/11/calculate-the-mortgage-interest-math.asp

- ↑ https://turbotax.intuit.com/tax-tips/home-ownership/deducting-mortgage-interest-faqs/L4a9KF9mI

- ↑ https://turbotax.intuit.com/tax-tips/home-ownership/deducting-mortgage-interest-faqs/L4a9KF9mI

- ↑ https://www.irs.gov/publications/p936

- ↑ https://www.investopedia.com/articles/mortgages-real-estate/11/calculate-the-mortgage-interest-math.asp

- ↑ https://www.irs.gov/publications/p936

- ↑ https://www.irs.gov/publications/p936

- ↑ https://www.irs.gov/publications/p936

About This Article