This article was co-authored by wikiHow Staff. Our trained team of editors and researchers validate articles for accuracy and comprehensiveness. wikiHow's Content Management Team carefully monitors the work from our editorial staff to ensure that each article is backed by trusted research and meets our high quality standards.

There are 8 references cited in this article, which can be found at the bottom of the page.

Learn more...

Corporate bonds allow you to invest in a company by lending it money rather than by buying a stake in its success, as you would if you bought stock in the company. Bonds are generally less volatile than stocks, which can make them a good way to balance a stock-heavy investment portfolio. Although bonds typically require a larger initial investment than stocks do, you can get around that with exchange-traded funds (ETFs), which allow you to buy small shares of many different bonds at once. Additionally, because ETFs are traded on the market just like stocks, they're more liquid than individual bonds.[1]

Steps

Method 1

Method 1 of 3:Choosing Bonds to Buy

-

1Look for investment-grade bonds trading on the market. Investment-grade bonds are generally considered less risky than non-investment grade bonds. You can find these bonds listed at any major financial website or paper, such as Barron's or the Wall Street Journal.[2]

- Stay away from anything that isn't classified as an investment-grade bond, especially if you're a beginning investor.

- You may also see non-investment grade bonds called "junk bonds" or "high yield bonds." While calling a bond "high yield" may sound more enticing than calling it "junk," these terms refer to the same type of bond. Remember that with a higher yield (the rate of return for a bond) comes higher risk.

-

2Check the company's creditworthiness with scores from ratings agencies. A bond is classified as investment-grade according to the company's credit score, but your investigation into the company's creditworthiness shouldn't stop there. The ratings agencies Moody's, Standard & Poor's, and Fitch all evaluate bonds and provide a specific rating for each bond issued. the higher the rating, the more likely the company is to pay back their debt.[3]

- The highest rating for bonds is AAA. Bonds rated AAA typically carry the lowest interest rates, which means less income for you over the lifetime of the bond, but it also means you're all but guaranteed to get your full investment back when the bond matures.

- Lower-rated bonds typically have higher interest rates, but they also have a higher rate of default.

Advertisement -

3Divide the company's operating income by its interest expense. Look up the 10-K filings of any company you're interested in buying bonds for. These will typically be available on the company's corporate website. You can also find them on the website of the US Securities and Exchange Commission (SEC) at https://www.sec.gov/edgar/searchedgar/companysearch.html.[4]

- Find the line with the company's annual operating income and divide it by the amount on the interest expense line. If your answer is 4 or higher, the company shouldn't have any trouble at all paying the bond. If your answer is below 2.5, the risk of default is pretty high.

- Do this calculation for 5 or 6 years to fully evaluate the overall picture of the company's financial health. If you just base your decision on one year, you run the risk that you're looking at a random off year or an uncharacteristically good year.

-

4Compare categories of corporate bonds. Corporate bonds are organized into categories that describe how the bond pays interest to bond investors. Choose the category that works best for your investment needs. While there are numerous sub-categories, the most common categories you'll encounter are:[5]

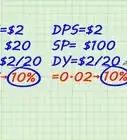

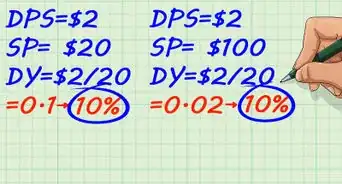

- Fixed rate bonds, which pay a fixed percent interest over the life of the bond. Payments may be made on a monthly, quarterly, bi-annual, or annual basis. For example, a $1,000 corporate bond with a 5% fixed rate would pay you $50 a year.

- Variable rate bonds, on the other hand, adjust interest rates to match the prime rate or some other benchmark. They pay out the same as fixed-rate bonds. While less reliable, you could potentially make more money off of variable-rate bonds than fixed-rate bonds.

- Zero coupon bonds do not make regular monthly, quarterly, bi-annual, or annual payments of interest. Rather, you get all the interest you earned in a lump sum on the maturity date of the bond. These are typically offered at a discount relative to fixed-rate and variable-rate bonds.

-

5Research initial bond offerings. If you're a beginning investor, initial bond offerings are likely out of your reach. These events are typically invite-only affairs for financially privileged investors who have an established relationship with the financial institution that's making the offering. However, it doesn't hurt to research. You can typically get a discount off the face value of the bond, although you may have to buy multiple bonds to get the discount.[6]Advertisement

Method 2

Method 2 of 3:Buying Individual Bonds

-

1Choose a broker that trades bonds on the secondary market. If an initial bond offering is out of range for you as an investor, you can still buy individual bonds on the secondary or "over-the-counter" (OTC) market. Most major brokers trade in the secondary bond markets.[9]

- If you're new to investing, look for a broker with a straightforward, intuitive platform and lots of guides and educational content aimed at beginners.

- You also want to compare the fees charged by brokers, as well as the minimum balance requirements. Some brokers lower or eliminate fees if you fund your account with an initial amount, such as $5,000 or $10,000.

Tip: Keep in mind that if you want to buy individual bonds, you'll typically need several thousand dollars to start. If you want to take advantage of initial bond offerings, you may need $10,000 or more.

-

2Open a brokerage account if you don't already have one. Once you've found a broker you want to use, you can open an account online in just a few minutes. You'll need basic identification information as well as your bank account information so you can fund your investment account.[10]

- Opening a brokerage account is similar to opening a bank account, and typically can be done entirely online in 10 or 15 minutes. However, keep in mind it may take a few days up to a week for a transfer of funds to complete so you can begin trading.

- If you already have a brokerage account, chances are your current broker trades bonds on the secondary market. While you still want to check their fees per trade, you may find it easier to keep your entire portfolio in one place, rather than using multiple brokerage firms.

-

3Identify the bonds you want to buy on your broker's platform. Once you're on your broker's platform, you can search the bond offerings on the secondary market to find the ones you've already researched and want to buy. You may also see different bonds that strike your interest that you hadn't looked at before.[11]

- If you're thinking about a different bond that you haven't researched before, check the company's creditworthiness and the rating of the bond. Make sure they match your investment needs. Lower-rated bonds may produce higher interest yields, but they also entail a much greater risk that the company will default and you won't get your initial investment back.

-

4Double-check the bond price to determine the markup. Many brokers offer "commission-free" bond trades, but the fees are baked into the price at which they offer the bond. Look up the latest quote for the bond and compare that to the price offered on your broker's platform. If your broker is offering the bond at a significantly higher price, you may want to rethink whether you're willing to pay that price.[12]

- You can also use the Trade Reporting and Compliance Engine (TRACE) at http://www.finra.org/industry/trace to look at all the OTC transactions on the secondary bond market for that particular bond. That will give you a better idea of how the price your broker has listed stacks up to what other people are paying for the bond.

-

5Place your order for the bonds you want to buy. The process for buying individual bonds is a little different than the process for buying stocks. You'll probably need the CUSIP number, which is a unique 9-digit number assigned to each bond traded on the secondary market. You may also need to provide additional information, such as the credit rating or the maturity range.[13]

- You can also provide price restrictions, such as whether you're willing to pay more than the face value or want the bond at a discount.

- Some brokers may require you to buy a minimum quantity of individual bonds. Check this quantity before you place your order to make sure you have the funds available.

Advertisement

Method 3

Method 3 of 3:Using Exchange-Traded Funds

-

1Find an ETF broker. Most major brokerage firms trade ETFs, so you shouldn't have any trouble finding a broker you like. If you already have a brokerage account, your current broker probably has ETFs available that you can choose from, so you don't have to worry about opening up another brokerage account.[14]

- It still may be a good idea to look around and see what kind of ETFs are available. Since you want to buy corporate bonds, it doesn't make a lot of sense to buy ETFs from a broker if that broker doesn't have much of a selection of ETFs that include corporate bonds.

-

2Fund your account if necessary. If you have a new account, you'll have to transfer money from your bank account so you can purchase ETF shares. Even for an established account, you'll likely need to add cash if you want to buy ETF shares.[15]

- Looking at the available ETFs and their average pricing can give you a good idea of how much money you need to fund your account.

Tip: It can take anywhere from 3 to 7 business days to complete a transfer from your bank to your brokerage account. If it's your first time funding your account, or if you're making a large transfer, it may take longer to complete.

-

3Look for commission-free ETFs with corporate bonds. Since ETFs are traded on the stock exchange, most brokers charge a commission on the shares you buy through them. However, many popular online brokers offer a range of ETFs that trade commission-free.[16]

- If you can find commission-free trades, you can potentially save a lot of money, especially if you're thinking about buying a significant number of shares.

-

4Place your order for the ETF shares you want. Once you've chosen the ETFs you want to purchase, you can place your order in the same way you would place an order for stock. ETFs have stock ticker numbers, but with most online brokers you can also search by name.[17]

- You can place a market order for however many shares you can get for a set amount of money, and you'll get your shares at whatever rate they happen to be trading for on the market at that moment.

- If you place a limit order, you're asking to buy a specific number of shares and setting the maximum price you're willing to pay for each share.

Advertisement

Warnings

- This article discussing buying corporate bonds in the US. If you live in another country, the process may be different. Talk to a local broker or investment advisor.Thanks!

- Even though bonds may be safer than stocks, they still carry the same inherent risks as any investment. The higher the yield promised by a bond, the higher the risk that the company will default on the bond. Never invest more than you are willing to lose.Thanks!

-Step-10.webp)

References

- ↑ https://www.nerdwallet.com/blog/investing/how-to-buy-bonds/

- ↑ https://www.investor.gov/introduction-investing/basics/investment-products/corporate-bonds

- ↑ https://www.nerdwallet.com/blog/investing/how-to-buy-bonds/

- ↑ https://www.nerdwallet.com/blog/investing/how-to-buy-bonds/

- ↑ https://smartasset.com/investing/how-to-buy-corporate-bonds

- ↑ https://smartasset.com/investing/how-to-buy-corporate-bonds

- ↑ https://www.fidelity.com/fixed-income-bonds/individual-bonds/corporate-bonds/corporate-notes-program

- ↑ https://investor.vanguard.com/investing/online-trading/buy-sell-bonds

- ↑ https://investor.vanguard.com/investing/online-trading/buy-sell-bonds

- ↑ https://www.nerdwallet.com/blog/investing/what-is-how-to-open-brokerage-account/

- ↑ https://investor.vanguard.com/investing/online-trading/buy-sell-bonds

- ↑ https://www.investopedia.com/ask/answers/08/how-to-buy-a-bond.asp

- ↑ https://investor.vanguard.com/investing/online-trading/buy-sell-bonds

- ↑ https://www.nerdwallet.com/best/investing/brokers-etf-investing

- ↑ https://www.nerdwallet.com/blog/investing/what-is-how-to-open-brokerage-account/

- ↑ https://www.nerdwallet.com/best/investing/brokers-etf-investing

- ↑ https://www.nerdwallet.com/best/investing/brokers-etf-investing

About This Article